Table of Contents

1. Overview

The Paying Taxes indicator is one of the most complicated indicators and is different from the other Doing Business indicators. It focuses on a SME that has to prepare and file its return for taxes, and then also focuses on requesting a VAT refund and also making a corporate income tax correction.

South Africa ranks 54 out of 190 countries in the Doing Business 2019 Survey. It has made some good reforms for the past year and will rank much better.

2. Business Procedures

The business procedures are different to the other indicators as there are no steps that are actually recorded.

The procedures are based on a Tax Professional or Accountants process of filing a return and the post filing index is also based on specific calculations based on the case study provided the World Bank.

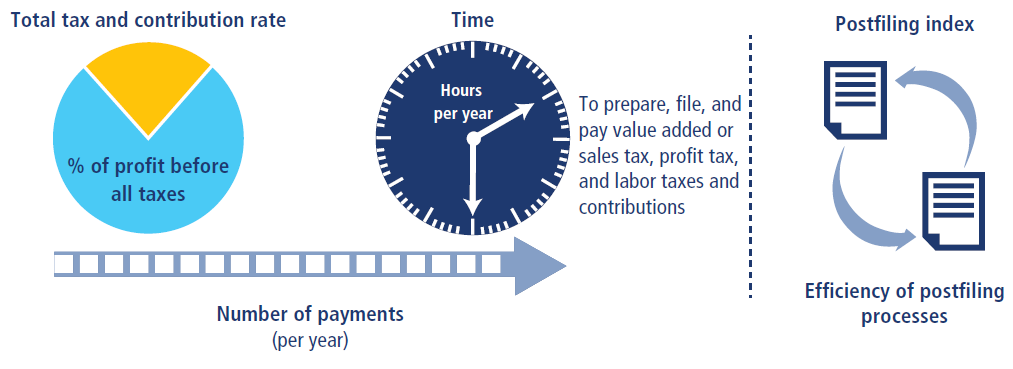

3. Methodology

Doing Business records the taxes and mandatory contributions that a medium-size company must pay in a given year as well as measures of the administrative burden of paying taxes and contributions and complying with postfiling procedures. The project was developed and implemented in cooperation with PwC. Taxes and contributions measured include the profit or corporate income tax, social contributions and labor taxes paid by the employer, property taxes, property transfer taxes, dividend tax, capital gains tax, financial transactions tax, waste collection taxes, vehicle and road taxes, and any other small taxes or fees.

4. Reforms

In terms of reforms, the tax authority or better known in South Africa as – SARS (South African Revenue Service) has to make reforms to make the laws simpler, make its systems and technologies easy to use so that a SME can file their returns and also make it easy for VAT returns. SARS is measured on its efficiency to conduct audits and also to make VAT refunds.

On the filing side, a Tax Professional or Accountant is also required to perform the filing functions in an efficient manner by making use of systems. The turnaround times for filing needs to be monitored more closely by the SME and Accountant so that the efficiencies are comparable to leading countries.

SARS has made the following reforms over the last Doing Business cycle.

1. Time to Comply – VAT Refund hours

The Paying Taxes Technical Working Group has engaged with the Professional Bodies (SAICA, SAIPA, SAIT) and the Tax Practitioners with regard to the understanding of obtaining the invoice for the one large capital asset. PWC was also requested to check with their counterparts in UK on their understanding. They were not ‘over interpreting’.

The outcome was that South Africa didn’t understand the case study well and realised that the invoice was already at hand in the Accounting System of the TaxPayerCo. In doing the previous VAT calculation, all the information was available, and only the one large invoice needed to be included.

This calculation time is in minutes and submission is done online (SARS efiling) which is also in minutes. The total time is therefore 30 to 60 minutes.

2. Time to obtain a VAT refund (weeks)

SARS has implemented reforms to ensure that their turnaround times for VAT refunds are Tax-filer centric.

a) The Service Charter was launched mid 2018 that expresses the service levels that SARS commits to. The Service Charter was launched to promote voluntary submissions and to improve the efficiencies of SARS. The Service Charter can be found here.

b) SARS is taking SME tax filers as a priority and has employed a SME Head to focus specifically in servicing the SME segment.

c) Research was conducted on VAT refunds by Prof Sharon Smulders. The results were presented to the Technical Working Group and SARS took note of the areas of improvement and worked on it.

d) SARS has conducted more than 3000 technical training sessions in the various tax products, including VAT, which contributed to the more efficient processing of VAT refunds. The executive management team, responsible for verifications and audits, has also successfully concluded an Executive Development Management Diploma.

e) SARS has a set of measures and targets in line with its Service Charter that is monitored tightly and is reported to the its executive leadership daily by means of live dashboards. The measures and targets are reinforced with Standard Operating Procedures.

f) SARS has continued to refine its risk rules, based on the hit rates reflected in historic data, as well as insights gained from audits and verification concluded. This resulted in significantly reduced intervention rates (>30% reduction) and consequently enabled SARS to elevate focus on a reduced audit and verification case load, which in turn resulted in increased efficacy.

g) By refining the risk rules and eliminating false positives, it automatically creates more capacity as there are fewer cases per auditor to work on. This improves turnaround times.

h) Communication: various communique on the VAT refunds were communicated. The Registered Controlling Bodies (Professional Bodies) are quite active and share the information with their members.

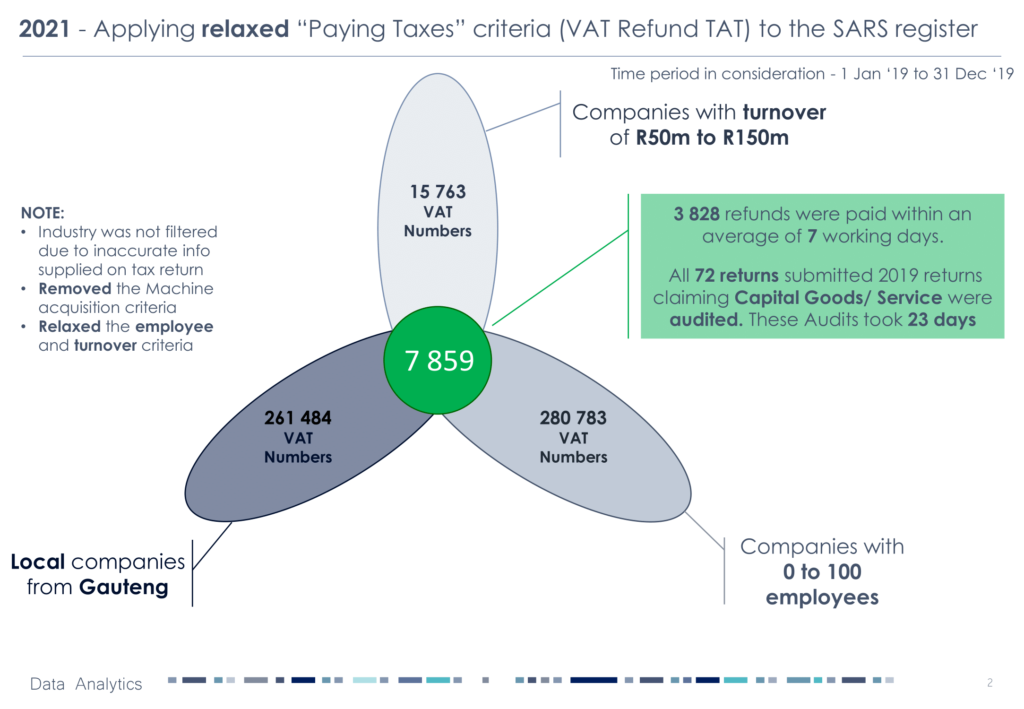

i) The data presented by SARS (empirical) showed 5 weeks (23 days) to obtain a refund. The Paying Taxes Technical Working Group shared their experiences of 4 to 5 weeks. The average processing turnaround times in days for VAT refunds was 23.17 in the previous year (2018). The unofficial, provisional number (yet to be made official in the annual report) for the financial year ending March 2020 is less that 19 21 days. SARS also has a differentiated risk management process, which responds to the risk profile and actual audit findings of its taxpayers – it is clear that the risk profile for medium sized companies, like the profile of the company in the DB case study, is slightly higher than the average of the total universe of VAT registrants. This is apparent from the average that applied in the data used for the purposes of the working group (23 days), as opposed to the overall SARS number of less than 19 days.

j) Risk Engine: In some cases, PWC observed that VAT refunds were done even before a verification. SARS response was that if the TaxPayerCo was in good standing and the probability of a sustainable going concern was high, then the VAT refund was paid whilst the verification was in progress. This is evident of SARS applying a differentiated risk management process.

Source: SARS Analytics Database

The data presented by SARS (empirical) showed 5 weeks (23 days) to obtain a refund.The Paying Taxes Technical Working Group shared their experiences of 4 to 5 weeks.

SARS allocation to the VAT account was increased in October 2018 and has since been continuously updated. Therefore, the VAT refunds has been fast.

In some cases, PWC observed that VAT refunds were done even before a verification. SARS response was that if the TaxPayerCo was in good standing and a going concern, then the VAT refund was done faster. Their risk was considered as low.

A reduction by 10 weeks to 5 weeks (from 15 weeks)

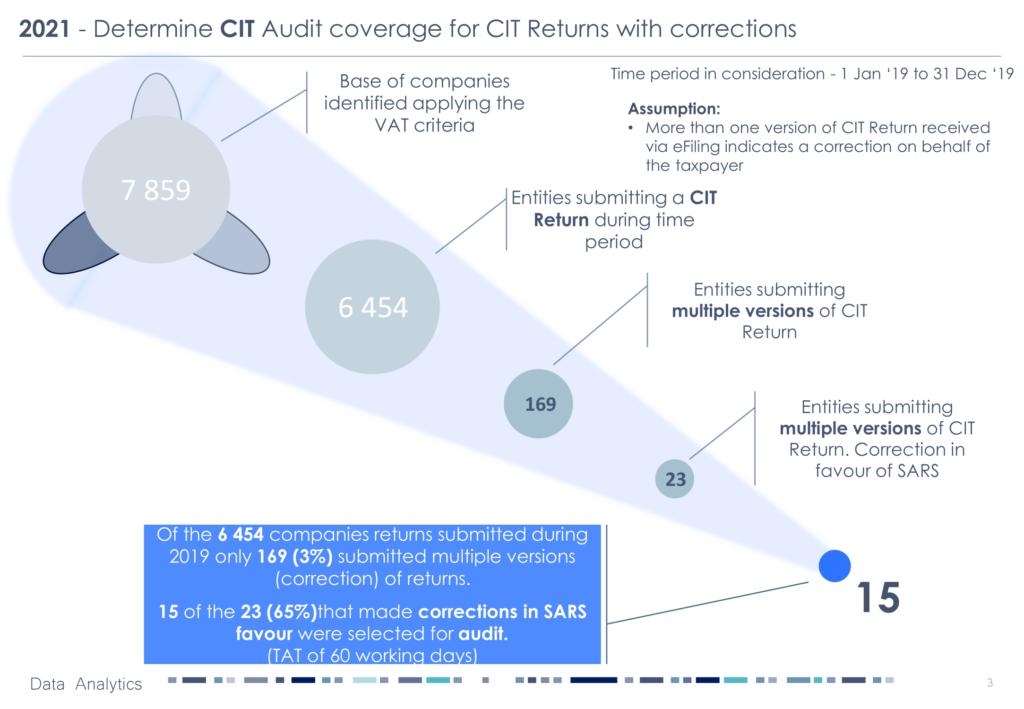

3. Time to complete a Corporate Income Tax Audit (weeks)

SARS has demonstrated that their time has significantly improved by placing emphasis (internally) to their audit division. This has resulted in an astounding improvement turnaround times.

Their audit division has received more training to improve its efficiency.

Source: SARS Analytics Database

A reduction by 15 weeks to 17 weeks (from 32 weeks)

5. Laws

6. Technical Working Group

The Paying Taxes Technical Working Group is chaired by a SARS Official and comprises of National Treasury, InvestSA, PWC, EY, SAICA, SAIPA, SAIT, IFC/World Bank Group.

7. Useful Links

8. Performance Statistics

10. Contact

Rebone Gcabo (PhD)

Head: Taxpayer and Trader Education Products

Email: rgcabo@sars.gov.za